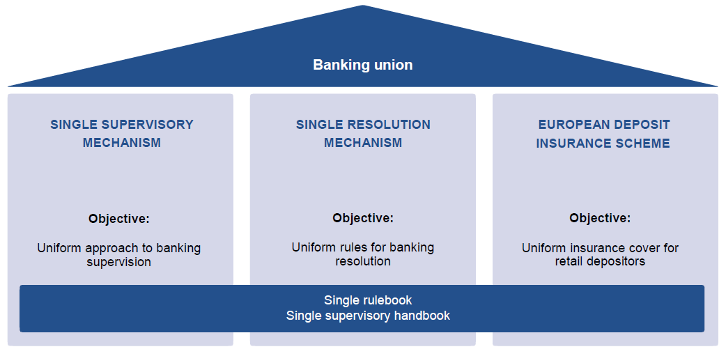

The three pillars of the banking union

The banking union is the biggest milestone in the integration of EU economies and institutions since the Economic and Monetary Union (EMU) was launched. It provides the essential underpinnings for financial stability and helps build crisis resilience and enhance risk monitoring and assessment. Moreover, the banking union addresses the fragmentation of financial markets within the euro area and contributes to breaking the negative feedback loop between bank debt and sovereign debt. The banking union benefits above all smaller countries with a large share of cross-border banking activities, such as Austria.

The banking union is based on three pillars:

- the Single Supervisory Mechanism (SSM)

- the Single Resolution Mechanism (SRM)

- the European Deposit Insurance Scheme (EDIS)

The first pillar of the banking union, the SSM, increases the effectiveness of supervision and enhances cross-border cooperation and coordination. Under the SSM, the European Central Bank (ECB) is responsible for the supervision of significant banks, i.e. of those banks on which the euro area’s financial stability hinges in the first place. The second pillar, the SRM, ensures an orderly resolution of failing banks. The proposal for the third pillar, EDIS, builds on the current system of national deposit guarantee schemes, which have been harmonized to ensure that all deposits are protected across the EU up to EUR 100,000 per person and bank. Ultimately, these bank deposit guarantees are to be fully financed by EDIS.

The consistency of supervisory practices within the banking union is ensured with the help of a single rulebook and a single supervisory handbook. Moreover, the ECB issues regulations, guidelines, recommendations and instructions for the banking system as a whole and is ultimately accountable for the effectiveness and consistency of the SSM.